Question

Vico Tony (VT) is a software design company established six years ago. The company is owned by five directors. Since establishment, the company has developed rapidly. VT finds it difficult to obtain bank finance and relies on a long-term strategy of using internally generated funds to finance expansion. The directors are therefore giving consideration to the possibility of floating the company on the stock market. As a first step, you have been appointed by the directors to advise on the current value of the business under their ownership.

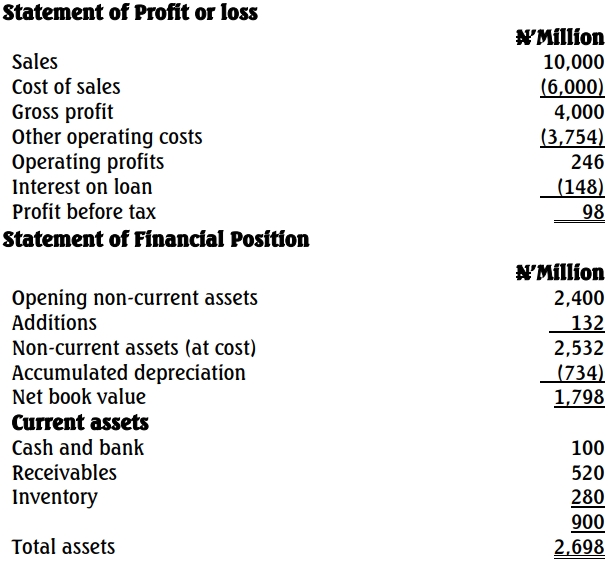

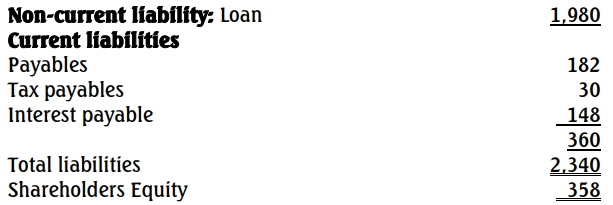

The company’s most recent statement of profit or loss and the extracted balances from the latest statement of financial position are as follows:

During the current year:

- Depreciation is charged at 10% per annum on the year-end non-current assets balance before accumulated depreciation, and is included in other operating costs in the statement of profit or loss.

- The investment in net working capital is expected to increase in line with the growth in gross profit.

- Other operating costs consisted of:

- Sales and variable costs are projected to grow at 9% per annum and fixed costs are projected to grow at 6% per annum.

- The company pays interest on its outstanding loan of 7.5% per annum and incurs tax on its profits at 30%, payable in the following year. The company does not currently pay dividends.

One of your first tasks is to prepare for the directors a forward cash flow projection for three years and to value the firm on the basis of its expected free cash flow to equity. In discussion with them, you note the following:

- The company will not dispose of any of its non-current assets but will increase its investment in new non-current assets by 20% per annum. The company’s depreciation policy matches the currently available tax allowable depreciation. This straight-line write-off policy is not likely to change;

- The directors will not take a dividend for the next three years but will then review the position taking into account the company’s sustainable cash flow at that time;

- The level of loan will be maintained at ₦1.98 billion and interest rates are not expected to change.

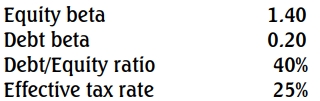

- For estimating the appropriate required return on equity, it is decided to make use of the capital asset pricing model (CAPM). The challenge, however, is that since the company is not quoted, an appropriate beta factor does not exist. You have found a listed company, Konputer Limited (KL) that is into software development. KL is also into computer hardware retailing. It has the following financial statistics:

- About 60% of the market value of KL is attributed to the software development division, while 40% of the value is attributed to computer hardware retailing. The computer hardware retailing division has an equity beta of 0.8.

- Risk-free rate is 4% and the market risk premium is 8%.

- VT has maintained a long-term debt/(debt+equity) ratio of 20%.

Required:

a. Provide an estimate of the appropriate rate of return to be used for the valuation of VT. Round your answer to the nearest whole number. (7 Marks)

b. Prepare a three-year cash flow forecast for the business on the basis described above highlighting the free cash flow to equity in each year. (14 Marks)

c. Estimate the value of the business based on the expected free cash flow to equity and a terminal value based on a sustainable growth rate of 4% per annum thereafter. (Note: Irrespective of your answer in (a), assume required return of 17%). (5 Marks)

d. Advise the directors on the assumptions and the uncertainties within your valuation. (4 Marks)